I was chudded yesterday so I waited a bit for that to expire before posting this.

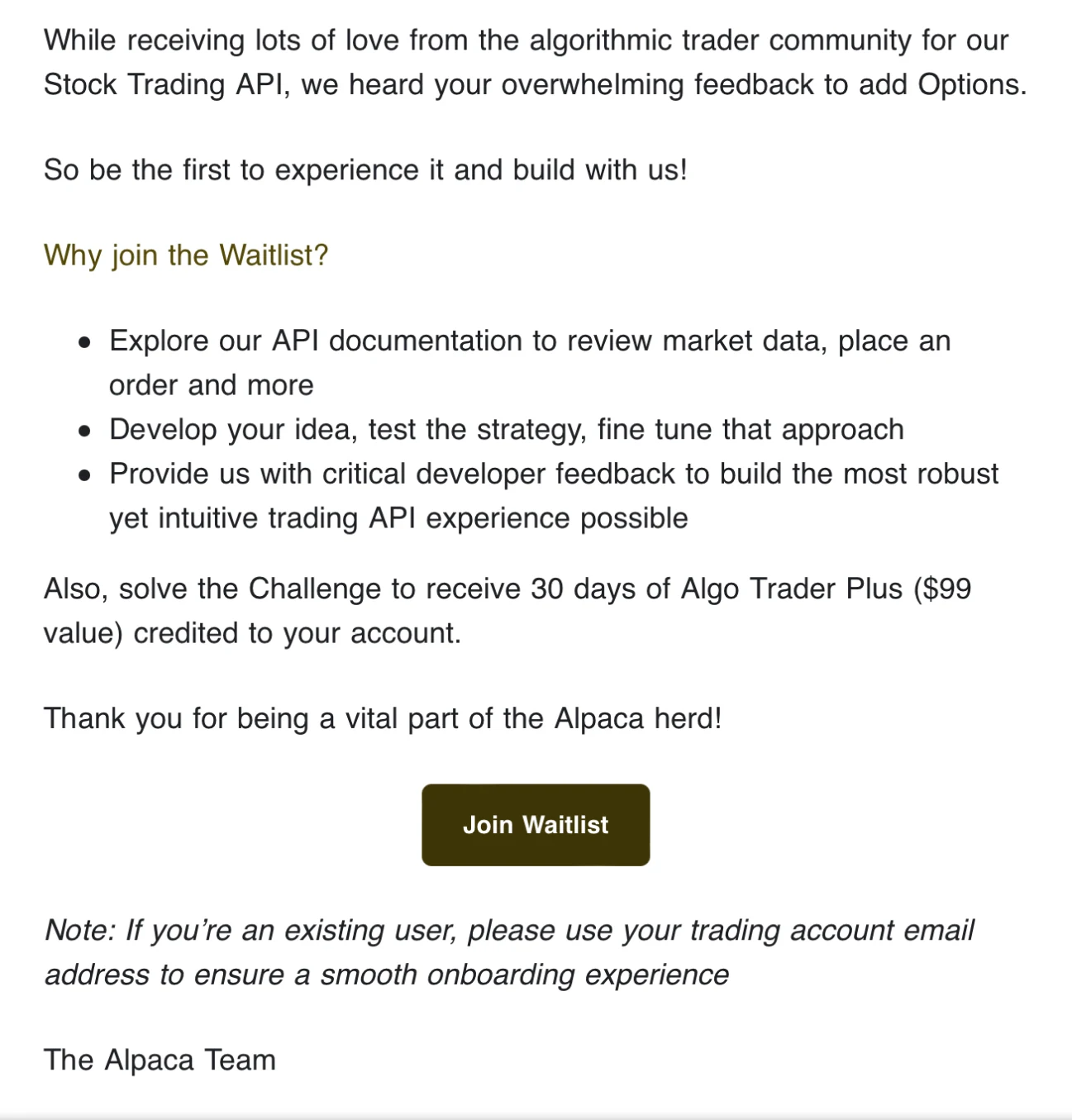

Alpaca is an API that allows you to algorithmically trade stocks. I've been wanting options for a long time, as most of my trading is theta ganging options. There has never really been a good API available to the average person for trading options till now. So much potential degeneracy has been unleashed!

Jump in the discussion.

No email address required.

Being a solo algo trader is like setting Tesla on autopilot using one of those rubber hands to keep it activated, plugging in a destination 10 hours away that goes through numerous metros, and then getting in the backseat to watch a movie.

Adding options to this is doing the same, but setting the cruise speed to 150 and filling the cabin with gasoline and fireworks

Jump in the discussion.

No email address required.

if you find a market inefficiency that's both big enough to overcome your trading costs (which are high compared to what the professionals pay), and small enough that the professionals aren't interested in it. (or perhaps if you find a market inefficiency that the professionals can't exploit for regulatory reasons, or don't want to exploit for accounting reasons.)

theta decay is not a market inefficiency.

Jump in the discussion.

No email address required.

Ah yes, the "pick up pennies in front of a steamroller" strat. Very stable and sure to bea the S&P 500 with minimal work on your end

Jump in the discussion.

No email address required.

that's the opposite of what I said. With "picking up pennies in front of a steamroller"-strategies you have no chance against the pros.

Jump in the discussion.

No email address required.

Well, typically those strategies the pros aren't using are because the risk is so high. Look at the WSB classics like the infinite leverage short box spreads

Jump in the discussion.

No email address required.

First of all:

I'm not saying you can find something like that. I'm saying algotrading only makes sense if you have found something like that.

But this is the kind of situation I meant:

1. you found a way to bet $10k for a 2:3 chance to get back $4k (lose $6k) and a 1:3 chance to get back $25k (gain $15k), aka the expected return is $1000. So the expected return of 1000 consecutive bets is $1M. (if the bets are iid, the probability that in the course of those 1000 bets you're at any moment down more than -$200k is 1.1%, the probability that you're ever down more than -$300k is 0.2%. The probability that at the end, after the 1000 bets, you're down at all is only 0.04%, the probability that at the end you're up at least $300k is 99%)

2. it doesn't generalize to a large class of underlyings. you can only make those bets ~4 times a day.

3. it doesn't scale in volume: the order books for the necessary trades are almost empty -- if you want to bet more than $10k the corresponding trades get rapidly more expensive, when betting $20k the expected return is already negative.

4. it would take a couple rentec level employees at least a month to figure out how to find this type of bet and to implement it in their system.

That's the kind of inefficiency that's too small for the pros, but it's ideal if you have $800k in your brokerage account.

Jump in the discussion.

No email address required.

Jesse what the frick are you talking about??

Jump in the discussion.

No email address required.

More options

Context

More options

Context

More options

Context

More options

Context

More options

Context

More options

Context

fwound the incwl

Jump in the discussion.

No email address required.

More options

Context

More options

Context